Mistakes Happen: Why Zero Off-Channel Isn’t Realistic

Mistakes happen. Pretending otherwise is how you get blindsided.

Most firms try to ban off-channel messages. Lock down WhatsApp. Block Signal. Tell people, “don’t text.” You can do all that and still get a Friday-afternoon screenshot you wish you didn’t see. Regulators know this, too. The win isn’t zero mistakes; it’s how you respond when they happen.

What I Mean by an “Oops Culture”

An “oops culture” is a safe, stigma-free way for employees to raise their hand when they slip up—fast.

Take two possible paths:

Path 1: The Oops Culture Way

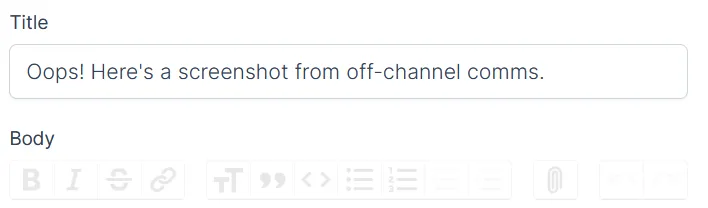

- Someone realizes they texted a client off-channel.

- They drop a screenshot or paste the text into your Oops Bot (open a case)

- The submission instantly opens a case. No extra steps, no chasing.

- It’s automatically archived for review

- They get recognition for surfacing the issue, not punishment for hiding it.

👉 Small “oops” now > big enforcement later.

Path 2: The Old Way

- Someone realizes they texted a client off-channel.

- They ignore it — or try to cover it. Maybe they say, “Hey, let’s move this to email.”

- The client thinks, uh, okay… that was easier, but fine.

- The original message? Not captured. Not archived.

- Will it get caught? Maybe. But if it does, it’s a bigger problem.

Which path would you rather your team take?

From Oops to Outcome: Case Management Inside Compliance Software

Self-reporting is step one. Structured follow-up is where the real value lives.

That’s why modern compliance software needs built-in case workflows. It’s not just about archiving messages. It’s about turning slip-ups into trackable, resolvable cases that regulators can see.

- Open a case instantly—from the message itself or from scratch. Easily attach the message.

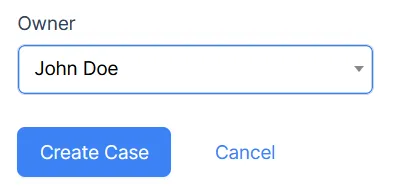

- Assign an owner (CCO, compliance lead, whoever is accountable)

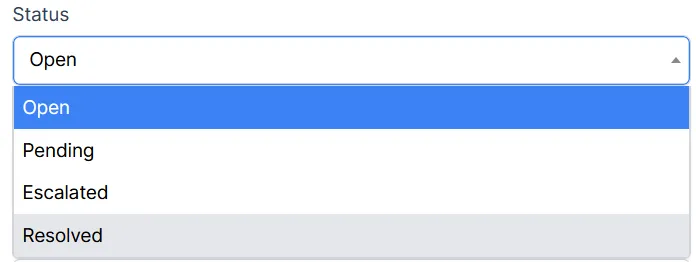

- Track status (open / pending / escalated / closed)

- Capture the resolution (policy tweak, process fix, informal/formal notice, suspension, termination, other)

- Link related cases to spot patterns across teams or reps

- Export clean reports for SEC/FINRA requests or board updates.

Keep the case editable until resolution so context isn’t lost. Once it’s closed, it’s locked - defensible, auditable, regulator-ready.

Why Regulators Care About More Than Policies

Paper policies don’t impress anyone anymore. Demonstrated supervision does.

Firms that pair an “oops culture” with compliance and risk management software show regulators they’re not just preventing problems, they’re actively managing compliance risk with accountability and transparency.

An oops culture + cases shows:

- Proactive oversight: issues get raised before they snowball.

- Clear accountability: every case has an owner and a timeline.

- Continuous improvement: outcomes feed real policy and process changes.

That’s how you move from defensive to trust-building compliance. (Yeah, that thing I keep mentioning: transparency = trust.)

Getting Started: Building an Oops Culture in Your Firm

- Lower the bar to report. Bot, form, Slack - whatever removes friction. Screenshots? Sure.

- Recognize honesty. Reward early reporting. Don’t make people regret being candid.

- Turn every oops into a case. Track it, assign it, resolve it.

- Close the loop. Share what changed. People report more when they see it matters.

Quick Reality Check: Compliance Isn’t About Perfection

Perfect compliance is a myth. Transparent compliance is achievable.

Culture alone isn’t enough. Pair it with the right tech -call it compliance risk management software, call it GRC software- and suddenly “oops” moments become proof points of accountability, not liabilities. And, let’s go one step further. Start capturing all the comms you know your team is using - because it’s not just email- and suddenly? You’ve got a lot less clean up.

If something’s off in this approach at your firm, let’s talk it through. There’s always a way forward.